Standard home insurance is meant to protect average priced homes with basic to semi-custom finishes. Custom or luxury homes have most likely outgrown a standard home insurance policy. That is where high value home insurance comes in… A high value home policy provide more coverage with unique benefits specific to luxury homes that a standard home policy is not designed to do.

Are you putting your biggest asset at risk by insuring it in the wrong caliber of insurance policy?

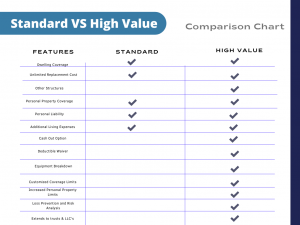

What are the major differences between a standard home policy and a high value home policy?

- Guaranteed Replacement Cost: Guaranteed replacement cost gives you an unlimited rebuild amount in the event of a total or large loss. Example: If your home rebuild coverage lists $1.2 million on your policy documents and you have to rebuild and it ends up costing $1.8 million. The insurance company will pay the $1.8 million regardless, of the rebuild coverage listed on your policy documents. A standard market insurance policy will discontinue coverage once the policy limit is exhausted.

- Cash Out Option: A high value home policy gives the insured the option to take a cash settlement instead of rebuilding their home. A standard home policy will require the home is rebuilt or damage is repaired with no cash out option.

- Deductible Waiver: High value home policies tend to carry higher deductibles (Such as $10K). In the event of a large claim (typically $50K or more) the insurance company will waive the $10K deducitble on your policy. A standard home policy does not provide the option to waive your deducitble regardless of the size of the claim.

- Equipment Breakdown: Luxury homes typically have luxury appliances and equipment. High value home policies come with equipment breakdown coverage to protect the breakdown or malfunction of those luxury appliances. Example: If you have a subzero commercial grade refrigerator that stops working and you need to replace it. It can cost $18K to purchase a new refrigerator and another $3K for installation. Your high value insurance policy would pay the full cost to replace that refrigerator and installation costs. Bonus*** it also only carriers a $500 deductible! A standard home insurance policy does not naturally come with this coverage. It sometimes can be added to your policy at an additional premium.

- Customized Coverage Limits: A high value home policy gives you the option to customize your coverage limits to best insure your unique custom home. Have you made a large investment in your landscaping? You can increase that coverage! Most standard home insurance policies come with package limits with restrictions on what you can adjust.

- Increased Special Personal Property Limits: A standard home policy typically has reduced limits for specific personal property items. A high value home policy increases these limits or reduces the limitiation all together.

Jewelry: $2,500 Standard Policy Limit vs. $25,000 High Value Limit

Firearms: $1,500 Standard Policy Limit vs. No Limit on High Value

- Loss Prevention and Risk Analysis: High value home insurance companies will provide you loss prevention services such as: preventative wildfire spraying, water detection and leak protection devices, or personal property inventory resources.

These are only the major differences between a standard home policy and a high value home policy. There are several other differences and benefits not outlined.

If you would like to discuss if your home should be insured as a high value home please request a review at Request a New Insurance Policy Quote